"He gets his allowance and it's gone in five minutes. Every. Single. Time."

You've explained budgets. You've explained saving. You've shown him the empty jar. And still — the moment money appears in his hands, it disappears. This is not a willpower problem. This is not a parenting problem. For children who think in concrete terms, money is invisible — and invisible things cannot be managed.

K-913

Life Skills & Independence

Financial Planning · Age 5–14

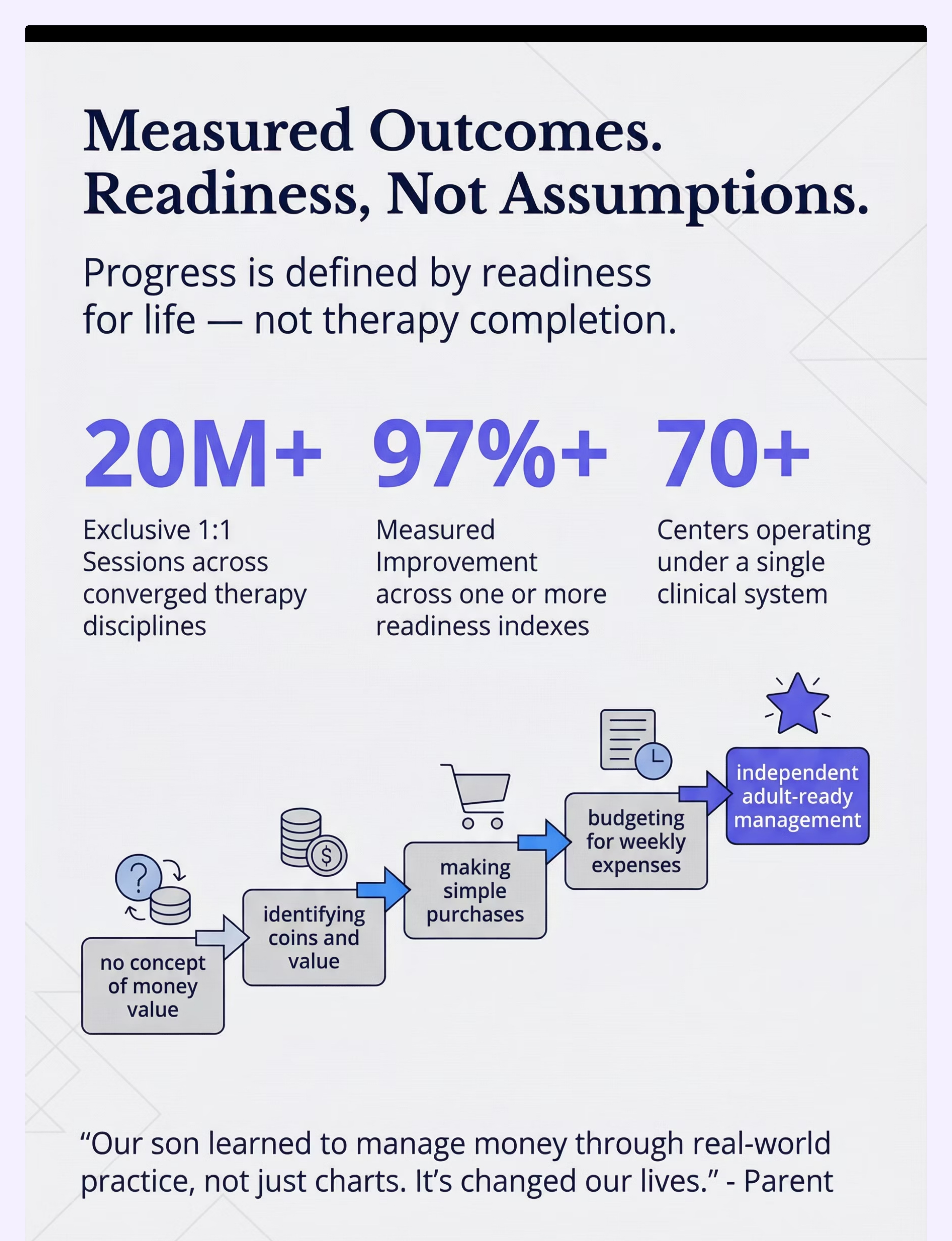

You are not failing your child's future. Their brain needs money to be visible, tangible, and experienced — not explained. That's exactly what these 9 materials do.

📞FREE National Autism Helpline: 9100 181 181 | 16+ languages | 24×7 | pinnacleblooms.org

Financial Literacy Is the Life Skill Most Families Are Not Taught to Teach

1 in 3

Never Receive Training

Children with developmental differences who never receive explicit money skills instruction

72%

Report Difficulties

Of autistic adults who report significant difficulties managing independent finances

₹0

Most Effective Tool

Cost of the most effective financial teaching tool — a clear glass jar with a goal picture

Globally, over 285 million children aged 5–14 are growing up without structured financial literacy exposure. For children with autism, ADHD, intellectual disability, or executive function challenges, the gap is even steeper — because standard financial education assumes abstract reasoning capacity that many of these children are still developing.

India has 18 million+ children with developmental differences. The majority will reach adulthood without the money management skills required for even basic independence. This is preventable. Concretely, practically, today.

Council for Economic Education (2024) | National Financial Educators Council | WHO Care for Child Development Package | PMC9978394

Why "Just Save It" Makes No Sense to a Concrete Thinker

The Problem Is Symbolic Abstraction

Money is purely symbolic. A ₹500 note has no intrinsic value — it represents a social agreement about purchasing power. For neurotypical adults, this symbol-to-value mapping is automatic. For children with autism, ADHD, or executive function challenges, the prefrontal circuits that create this abstract mapping are still developing — or are wired differently.

This is wiring, not willpower.

Three Cognitive Challenges at Play

Symbolic Reasoning Gap

A ₹10 coin and a ₹500 note look different but neither looks like what it can buy. Children who think concretely need the connection made visible.

Delayed Gratification Barrier

"Save for three weeks" requires holding a mental representation of a future reward — a working memory demand that challenges many children with developmental differences.

Finite Resource Concept

Digital cards appear to produce unlimited money. Without seeing a jar empty or coins physically disappear — "can't afford" is genuinely opaque.

Frontiers in Integrative Neuroscience (2020): DOI 10.3389/fnint.2020.556660 | Executive function development (Diamond, 2013)

Financial Understanding Develops in Stages. Here's Where Your Child Is.

For children with developmental differences, each stage may span 2–3× longer. This is normal. The materials on this page work at every stage.

Ages 3–5

Coins have names. Money exchanges for things. Key materials: Play money, piggy banks, pretend stores

Ages 6–8

Values & counting. Saving is possible. Earn through tasks. Key materials: Clear savings jars, earning charts, price cards

Ages 9–11

Budgeting basics. Trade-off decisions. Key materials: Budget charts, Save-Spend-Give dividers, shopping games

Ages 12–14

Opportunity cost. Banking. Planning. Key materials: Full budgeting tools, real account management

Children with autism, ADHD, intellectual disability, or executive function challenges typically progress through these stages at 1.5–3× the typical timeline. This is expected. This is not failure. This is your starting point.

WHO Care for Child Development (CCD) Package | UNICEF Developmental Monitoring Framework | PMC9978394

Clinically Validated. Home-Applicable. Parent-Proven.

🛡️ EVIDENCE LEVEL: STRONG

NCAEP 2020 Evidence-Based Practice

Study 1 — Visual Supports & Financial Learning

Children with autism who used concrete, visual financial tools showed significantly higher money identification and basic budgeting skills compared to verbal instruction alone.

Source: Occupational Therapy in Mental Health | Life Skills Development Literature

Study 2 — Delayed Gratification Training

Structured visual savings systems (clear jars with goal pictures) significantly improved delayed gratification tolerance in children with ADHD and ASD over 8-week intervention periods.

Source: Journal of Applied Behavior Analysis | Token Economy Literature

Study 3 — WHO Care for Child Development (CCD)

Home-based structured skill-building programs across 54 LMICs demonstrated that caregiver-delivered interventions using concrete materials are equally effective to clinic-based approaches for life skills acquisition.

Reference: PMC9978394

Study 4 — Indian Pediatric Context (Padmanabha et al., 2019)

Home-based structured interventions administered by trained parents showed significant developmental outcomes across adaptive behavior domains including life skills.

Reference: DOI:10.1007/s12098-018-2747-4 | Indian J Pediatr 2019

"Clinically validated by a consortium of OT, ABA, SLP, SpEd, and NeuroDev specialists. Home-applicable with materials costing ₹0–₹800. Parent-proven across 20M+ therapy sessions."

Financial Planning Materials for Children

K-913

Parent-Friendly Alias: "Making Money Real"

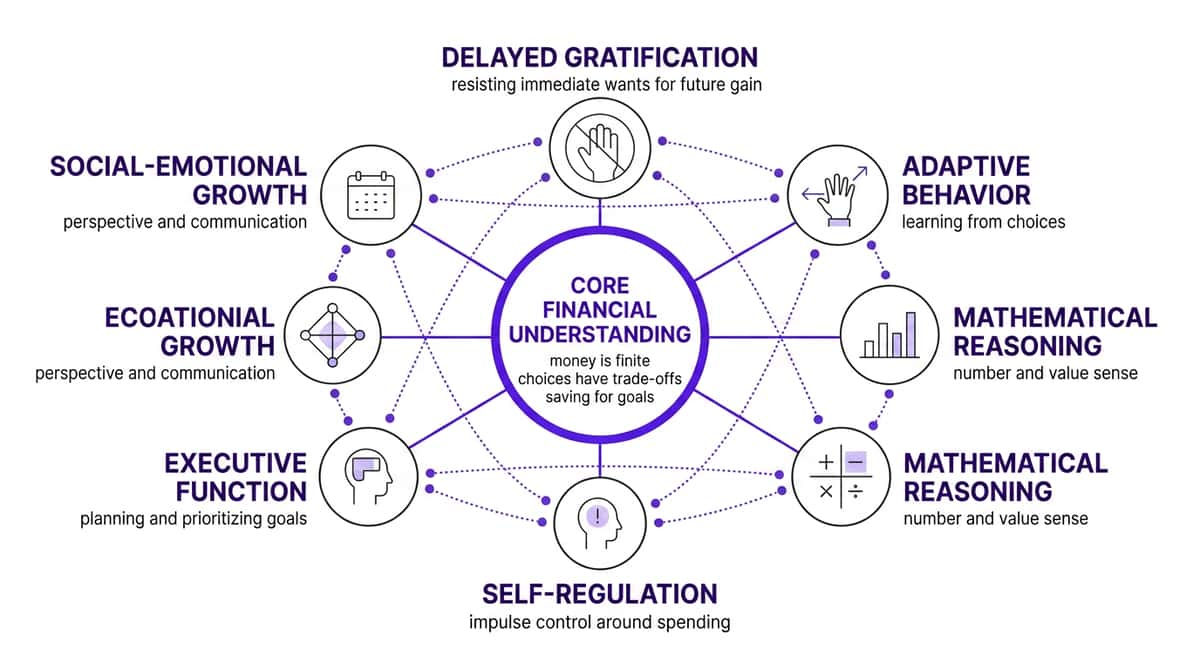

Financial literacy skills development through concrete, visual, hands-on materials is a structured approach to teaching children the concepts of earning, saving, spending, budgeting, and giving — by replacing abstract explanations with tangible, observable, manipulable experiences.

For children with developmental differences, this approach makes the invisible mechanisms of money management physically present: coins accumulate visibly in jars, budgets are moved as physical tokens, earning is tracked on boards, and time is counted down on calendars. Money management is not an academic subject — it is the foundation of adult independence.

Domain Badges

Life Skills

Executive Function

Adaptive Behavior

Mathematical Reasoning

Independence Skills

Specification

- 👶 Age: 5–14 years

- ⏱️ Session: 10–20 minutes

- 📅 Frequency: Daily (embedded in routine)

- 🏠 Setting: Home + Community + Clinic

K-913 is Episode 913 in the Parent & Caregiver Tools series. ← K-912: Insurance Navigation | K-914: Planning for Future → Browse all 999 Reels

This Technique Crosses Every Therapy Boundary

🦾 Occupational Therapist

Primary lead for financial life skills. OT addresses adaptive behavior and executive function components — sorting, categorizing, sequencing, and fine motor aspects of money handling. OT designs the environmental setup and material selection.

🗣️ ABA / BCBA Therapist

Token economy architect. ABA structures earning systems, reinforcement schedules, and behavior-to-reward chains. Delayed gratification training and impulse control around spending are core ABA targets.

📚 Special Educator

Math-to-life bridge builder. SpEd integrates mathematical reasoning components — coin values, addition, comparison, budgeting math — into functional real-world practice rather than worksheet arithmetic.

👨⚕️ NeuroDev Pediatrician

Developmental trajectory setter. Establishes the developmental baseline, identifies executive function profiles affecting financial learning, and monitors progress milestones.

"The brain doesn't organize by therapy type. A child learning to save money is simultaneously practicing executive function (OT domain), delayed gratification (ABA domain), mathematical reasoning (SpEd domain), and adaptive independence (NeuroDev domain)." — 🔄FusionModule™Active — OT + ABA + SpEd + NeuroDev coordinated protocol

This Is a Precision Tool, Not a Random Activity

Every session with these 9 materials is building toward a specific, measurable outcome — not just keeping children busy. The bullseye shows exactly what's being targeted at each level of engagement.

Target | What You'll See | Timeline | |

Money is finite | Child says "I don't have enough" with understanding | Weeks 2–4 | |

Trade-offs exist | Child hesitates, says "if I buy this, I can't buy that" | Weeks 4–6 | |

Saving is possible | Child adds to jar voluntarily, checks progress | Weeks 3–5 | |

Earning connects to money | Child asks what jobs are available when they want something | Weeks 4–8 | |

Value sense developing | Child distinguishes cheap vs expensive items correctly | Weeks 6–10 |

PMC10955541 | Meta-analysis — Life skills interventions across adaptive behavior domains (2024)

9 Materials That Make Money Visible, Tangible, and Teachable

These 9 materials work as a system. Each one targets a different dimension of financial understanding. Start with 1–2. Add more as your child progresses. Every material has a ₹0 DIY alternative (→ Card 10).

1. Clear Savings Jars With Visual Goals

Transparent containers where coins and bills accumulate visibly. Attach a photo of the desired item. Mark progress lines. The child can literally see their savings grow — transforming abstract saving into a physical experience.

Why it works: Visual feedback loop makes delayed gratification possible. 💰 ₹100–300 | 🛒 Shop on Amazon.in

2. Play Money & Coins Sets

Realistic play currency sets allowing unlimited practice with denominations, counting, making change, and exchange — all without real-money risk.

Why it works: Hands-on manipulation builds automatic coin/note recognition that transfers to real transactions. 💰 ₹150–500 | 🛒 Shop: ₹673 Canon Active SKU

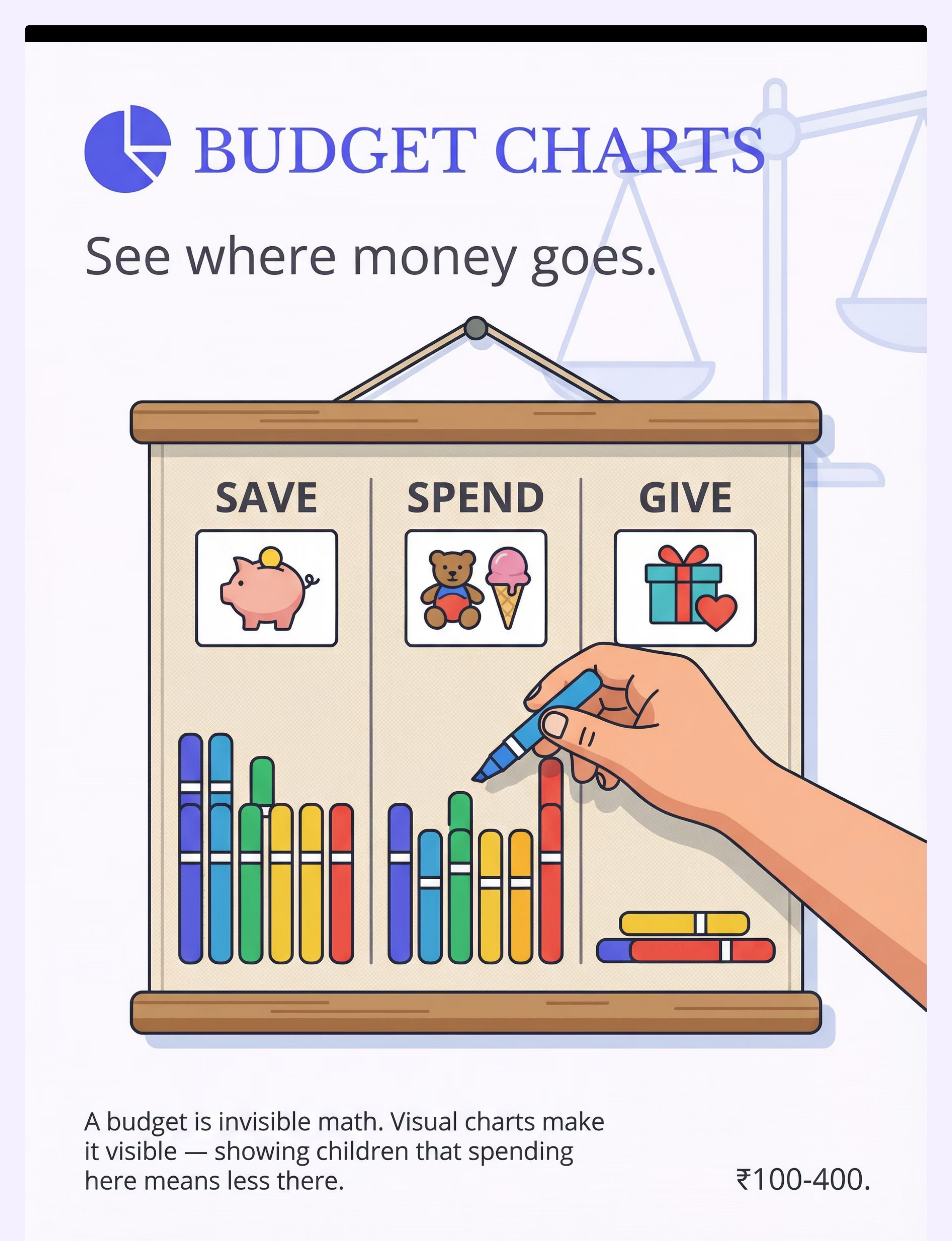

3. Visual Budget Charts

Chart with divided categories (Save / Spend / Give). Physical tokens move as money is allocated. Trade-offs become visible when one category fills and another empties.

Why it works: Budgeting is invisible math until it becomes visible movement. 💰 ₹100–400 | 🛒 Shop: ₹628 Canon Active SKU

📞 Need material guidance? Call 9100 181 181 — our OT team advises on material selection for your child's profile.

9 Materials — Continued

4. Save-Spend-Give Dividers

Three clear containers labelled Save (goal picture), Spend (wanted items), Give (heart). Every time money is received, the child physically divides it before spending anything.

Why it works: Ritual division prevents impulsive consumption and builds intentional money management from age 5. 💰 ₹200–600 | 🛒 Search Amazon.in

5. Price Comparison Cards

Cards showing items with prices. Child sorts from cheapest to most expensive, finds items within a budget, compares what the same amount can buy.

Why it works: Value sense develops through comparison, not explanation. 💰 ₹100–300 | 🛒 Shop: ₹296 Canon Active SKU

6. Earning Charts & Job Boards

Board listing tasks with payment amounts. Child marks completed jobs and watches earnings accumulate. Direct cause-effect between effort and reward.

Why it works: Children who earn money understand it differently than children who receive it. 💰 ₹50–200 | 🛒 Shop: ₹589 | Alt: ₹364

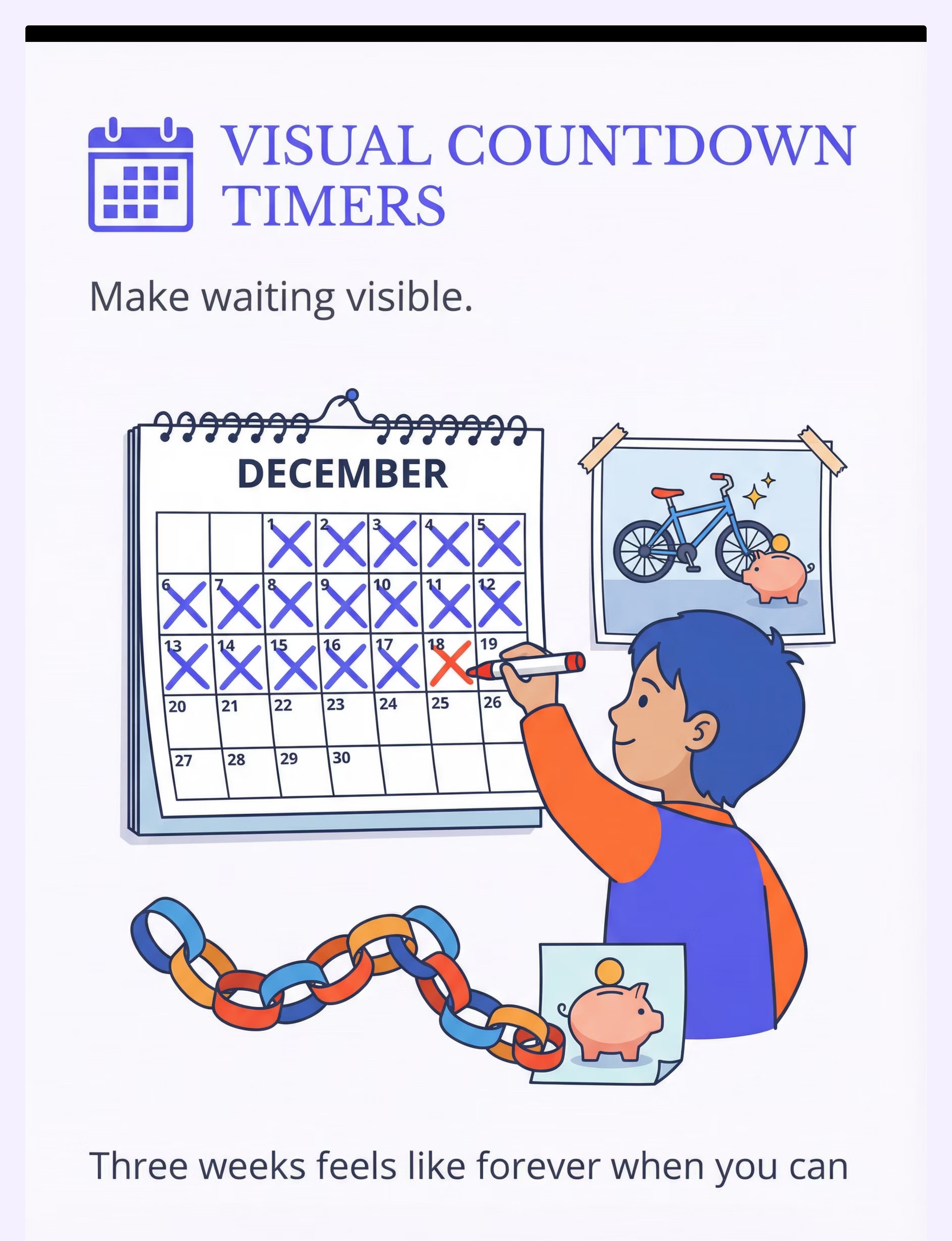

8. Visual Countdown Timers for Saving

Paper chains (one link per day), countdown calendars, progress charts. Shows exactly how many days remain and how much has been saved — making abstract time concrete.

Why it works: Delayed gratification requires representing future time. 💰 ₹50–200 | 🛒 Search Amazon.in

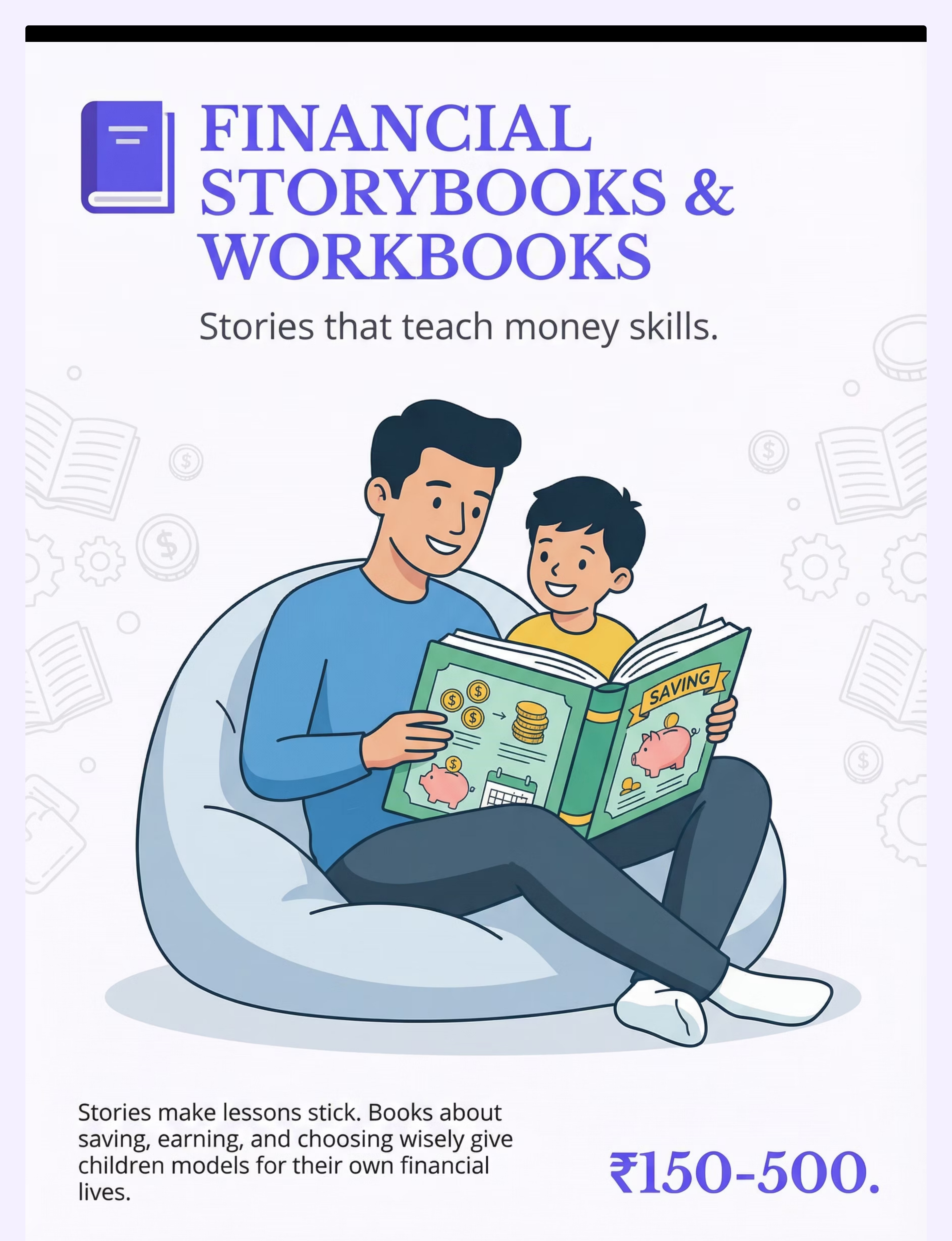

9. Financial Storybooks & Workbooks

Children's books about saving, earning, spending wisely, and generosity. Workbooks with money math and financial scenarios.

Why it works: Stories contextualize skills. Characters who navigate financial decisions provide frameworks children can adopt. 💰 ₹150–500 | 🛒 Search Amazon.in

Starter Kit Recommendation (₹500–800 total): Clear savings jar from home + printed goal picture (₹0) · Number/Counting Materials set (₹673 active SKU) · Three containers from home + labels (₹0) · Poster board earning chart (₹50) · Index card price cards (₹30)

Every Parent Can Do This. Right Now. With What You Have.

WHO/UNICEF equity principle: Every intervention on techniques.pinnacleblooms.org has a ₹0 version. Financial skill-building should not be gated by purchasing power.

Material | Buy Option | Make It Today (₹0) | Why It Works the Same | |

Clear Savings Jar | ₹100–300 | Any clear container from kitchen — old pickle jar, water bottle | Transparency is the mechanism. The container's job is to make accumulation visible. | |

Play Money Set | ₹150–500 | Print free templates from internet, laminate with tape | Realistic appearance enables transfer. Handling many transactions builds automaticity. | |

Budget Chart | ₹100–400 | Poster board + 3 columns drawn + paper tokens as coins | The physics of moving tokens matters more than the product. | |

Save-Spend-Give Dividers | ₹200–600 | 3 empty containers from kitchen (dabbas), add picture labels | Three containers = three purposes. The ritual of dividing is the intervention. | |

Price Comparison Cards | ₹100–300 | Index cards + cut pictures from newspapers/catalogs + written prices | The comparison activity drives value-sense. Pictures and prices are all that's needed. | |

Earning Chart | ₹50–200 | A sheet of paper with jobs + rupee amounts written in bold | Cause-effect is the mechanism. The visual record of work → earning is what teaches. | |

Shopping Practice Game | ₹200–800 | Set up items around home with paper price tags + play money | Real objects + real prices + simulated choice = identical learning. | |

Countdown Timer | ₹50–200 | Paper chain: one link per day. Remove link daily together. | Physical removal of a link makes time passing concrete and celebratory. | |

Financial Storybook | ₹150–500 | Create a personalized story: "Arjun saves for his bicycle" using your child's name/goal | Personal relevance dramatically increases engagement and retention. |

Zero-Cost Complete Kit: 3 kitchen containers + pickle jar + poster board + index cards + newspaper cutouts + paper clips for tokens = Complete financial learning environment. ₹0.

For children with significant sensory processing or fine motor challenges, your OT can specify clinical-grade materials. Contact: 9100 181 181

🔴 DO NOT PROCEED IF: Child is in a meltdown · Child is physically unwell or feverish · Child has had inadequate sleep · Child has severe intellectual disability requiring clinical-first approach (📞 9100 181 181) · Real money amounts exceed the child's current understanding · Child has severe impulse control issues previously resulting in unsafe behavior

Read This Before Every Session

🟡 Modify If:

- Child is mildly tired or slightly resistant today → Use shortened, simpler version (single jar activity only)

- Child has dyscalculia → Focus on categorical understanding before numerical amounts

- Child has anxiety around money → Keep activities playful, separated from family financial discussions

- Digital/card transactions are confusing → Use physical-only money system initially

🟢 Proceed When:

- Child is fed, rested, calm, and regulated

- Environment is set up (→ Card 13)

- Parent/caregiver is calm with 15–20 uninterrupted minutes

- Activity is presented as engaging play, not instruction

⚠️ Material Safety: Small coins are a choking hazard for children under 5 or those with oral-seeking behaviors. Use larger play coins. Use plastic containers with younger children. Supervise all cutting activities for DIY materials.

🔴 STOP IMMEDIATELY IF: Child becomes severely distressed or physically aggressive over money/items · Child begins hoarding behavior that creates distress · Child is unable to disengage (perseveration). Stop session. Note what happened. Contact your therapist. This is data, not failure.

Indian J Pediatr 2019 home safety protocols | DOI:10.1007/s12098-018-2747-4

The Right Environment Prevents 80% of Session Difficulties

Child Position

Seated comfortably at table or floor — same height as parent. Materials within easy reach. No chair restrictions that feel confining.

Parent Position

Beside child (not across). Slightly back to allow child agency. Hands ready to assist, not direct. Calm body posture throughout.

Materials Setup

Place only the materials for today's specific activity. Put away everything else. Reduce decision fatigue by limiting visible options to what's being used.

Goal Picture Visible

The item the child is saving for should be visible throughout the session — taped to the jar, pinned at eye level. This is motivational anchoring.

Distraction Removal

Remove screens/devices. Reduce visible toys. Close doors to reduce ambient sound. Inform other family members: "15 minutes, do not interrupt."

Environmental Settings

- Lighting: Natural light preferred. Avoid flickering fluorescent.

- Sound: Quiet or soft background music. No TV.

- Temperature: Comfortable — a physically uncomfortable child is a dysregulated child.

- Time of Day: After school snack or morning routine — when child is fed but not sleepy.

Key Principle

The environment is a therapeutic tool. A well-set-up space reduces the cognitive load of the session and lets the financial skill be the focus — not managing distractions.

60-Second Readiness Assessment — Before Every Session

Readiness Check

Complete Before Each Session

Fed?

Child has eaten within the last 2 hours. Hunger = low frustration tolerance.

Rested?

Child has had adequate sleep. Sleep-deprived children struggle with abstract learning significantly more.

Calm?

Child is in a regulated baseline state — not in recovery from a recent meltdown (allow 30–60 min buffer after any dysregulation).

Willing?

Child has shown a recent positive response to money/saving topics OR is in a generally cooperative mood.

Motivated?

The savings goal item is something the child currently wants. If interest has shifted, update the goal picture before starting.

Time?

Parent has 15–20 uninterrupted minutes. Sessions cut short are worse than sessions not started.

Count | Decision | Action | |

5–6 ✅ | 🟢 GO | Proceed to Step 1 (Card 15) | |

3–4 ✅ | 🟡 MODIFY | Single activity only (just the jar, 5 minutes) | |

0–2 ✅ | 🔴 POSTPONE | Use alternative calming activity. Revisit tomorrow. |

Not every day is a session day. Consistency means 4–5 sessions per week, not 7. A skipped day is not failure.

Step 1 of 6

⏱️ 1–2 minutes

Begin With Curiosity, Not Instruction

💬 "Hey [child's name], want to do something with your money today? I think your jar is getting pretty full — let's go check."

OR for a goal-focused child:

💬 "We're getting closer to [goal item]. Want to count how much you've saved? Let's see how far away we are."

Body Language Guidance

- Move toward the jar/materials first, without looking back — invite through movement, not demand

- Kneel or sit to child's eye level

- Relaxed, curious expression — not eager or pressured

- Have the goal picture visible before the child arrives at the table

Acceptance vs. Resistance Cues

✅ Child is joining willingly:

- Moves toward the activity independently

- Looks at the jar with interest

- Says yes or moves toward you

❌ Do not push through:

- Child moves away or says "no" clearly → Offer again in 10 minutes

- Child is distracted → Give "5 more minutes then money time" warning

ABA Pairing Principle: The first 60 seconds of every session establishes whether money = positive or money = demand. Protect this association fiercely.

Step 2 of 6

⏱️ 2–3 minutes

Introduce the Material With Child-Led Agency

Place the day's material in front of the child without instruction. Let them touch it, examine it, and respond naturally for 30–60 seconds. Then begin:

💬 "This is your savings jar. See this line? When the money reaches here, we can get [goal item]. Let's put today's money in."

For the Savings Jar

Let child hold coins before putting them in. Count together: "One coin... two coins... three coins." Let child drop each one in. Pause to listen to the sound. This sensory engagement locks the experience in memory.

For the Earning Chart

Point to the task completed: "You [did task]. That means you earned ₹[amount]. Let's put a star here and add it to your total." Let child make the mark and add the number.

For the Budget Chart

"You have ₹[amount] this week. Let's decide together where it goes. Save pile... spend pile... give pile." Place tokens in child's hands. Let them physically move tokens to categories.

🟢 | Engagement: Child is actively handling materials, looking, asking questions | |

🟡 | Tolerance: Child is present but passive — narrate and continue gently | |

🔴 | Avoidance: Child pulls away, leaves, protests — reduce demand, offer choice |

Reinforcement Cue: The moment child independently interacts with material (puts coin in, marks chart): "Yes! Look at that. You're saving!"

Step 3 of 6

⏱️ 5–10 minutes

The Core Financial Skill Being Built Today

Select the primary action based on your child's current developmental stage:

🔵 Stage 1 (Ages 5–7 / Early Learners): ACCUMULATION

Action: Child adds coins/notes to clear savings jar. Counts current total together. Looks at goal picture. Counts how many more needed.

Therapeutic mechanism: Visual accumulation + counting + goal connection = concrete saving concept

What to say: "Count with me. How many do we have? How many more until we reach the line?"

🟡 Stage 2 (Ages 7–10 / Developing): DIVISION

Action: Child receives weekly allowance. Physically divides into Save/Spend/Give containers using a percentage guide. Makes allocation decisions with support.

Therapeutic mechanism: Physical division + category decision + ritual = budgeting behavior pattern

What to say: "Half goes to saving. A little to giving. The rest you can spend. You decide."

🟢 Stage 3 (Ages 9–12 / Advancing): TRADE-OFF

Action: Child has budget card with ₹ amount. Selects from price comparison cards what to "buy." Discovers when budget runs out. Makes priority decisions.

Therapeutic mechanism: Limited resource + choice + consequence = trade-off understanding

What to say: "You have ₹50. These are your options. What do you want most? Does the money reach?"

🔴 Stage 4 (Ages 11–14 / Independent): EARNING SYSTEM

Action: Child reviews job board. Selects tasks for the week. Completes tasks, records earnings, makes spending/saving decisions with earned money.

Therapeutic mechanism: Effort-reward chain + earned autonomy = independent money management readiness

What to say: "Your money, your choices — but let's see the plan first."

Execution Precision: Use the child's own money or realistic token amount. Let the child physically handle every token/coin/note. Never rush the counting. If a mistake is made, gently recount — do not express frustration. PMC10955541 — Hands-on concrete manipulation for abstract concept development

Step 4 of 6

⏱️ 2–5 minutes

Repetition Builds the Neural Pathway. Variety Keeps It Engaged.

"3 Great Reps > 10 Forced Reps" — Pinnacle Clinical Principle

The goal is 2–4 meaningful repetitions, not unlimited drilling. Quality over quantity. Stop when child's engagement begins to drop — BEFORE they're bored.

Variation | What to Do | When to Use | |

Role Reversal | Child becomes the "bank" — parent asks to make a deposit | When child is very engaged — deepens understanding | |

New Goal Scenario | "If you were saving for [different item], how long would it take?" | When child has mastered current goal concept | |

Real Store Extension | Take budget card to actual small store, use it for one real decision | When child is ready for real-world transfer | |

Story Connection | Read one page of financial storybook between repetitions | When child needs a break but staying engaged |

Satiation Indicators — Stop Here: Child asks to do something else · Child begins fidgeting significantly · Quality of engagement drops (going through motions) · Child says "done" — HONOR THIS. Ending on their terms = next session begins willingly.

Step 5 of 6

⏱️ 1–2 minutes

Celebrate the Attempt. Always. Even Imperfect Ones.

Reinforcement Timing: Within 3 seconds of any desired financial behavior — counting correctly, making a division decision, adding to jar, choosing to save over spend.

For Correct Counting

💬 "Yes! ₹10, ₹20, ₹30 — you got it! That's exactly right."

For Division Decision

💬 "You decided to save half. That's a really smart money decision. I'm proud of you."

For Choosing to Save

💬 "You picked saving over spending right now. That is NOT easy. Well done."

For Reaching a Milestone

💬 "Look at that! You're halfway to [goal item]. Your saving is working!"

Reinforcement Menu Options

- Verbal praise (specific + immediate — always)

- High five / fist bump (if child accepts physical praise)

- Token on earning chart (if using token system)

- Sticker on savings progress chart

- 5 minutes of preferred activity immediately after session

- Special entry in "Money Journal" — child dictates/draws what they did today

ABA Principle

Reinforce the behavior (the saving decision, the counting accuracy), not just the outcome (the amount saved). This builds intrinsic understanding, not just outcome-chasing.

Do NOT offer food rewards for financial skill practice unless part of a formal ABA plan.

Step 6 of 6

⏱️ 1–2 minutes

No Session Ends Abruptly. Every Session Closes With Ritual.

💬 "One more, then we're all done for today." (Repeat: "Last one... almost done... let's put it away now.")

Child Puts Materials Away

Child participates in cleanup = session ownership. This reinforces permanence and value of the savings system.

Review Progress Together

"Let's look at how much you've saved total." Pause. Let child see/count.

Look at Goal Picture

"We're getting closer. [X] more days/coins." Keep anticipation alive.

Verbal Close

💬 "Great money work today. You're really getting good at this."

Transition to Next Activity

"Now let's [snack / play / rest]." Clear transition signal prevents perseveration on the activity.

If Child Resists Ending (a good sign — high engagement): Use countdown: "Three more coins, then we put the jar away. Three... two... one. Well done." Offer continuation tomorrow: "We can do more tomorrow. The jar stays safe overnight."

NCAEP (2020) Visual Supports Evidence-Based Practice: Transition supports including visual timers are classified as evidence-based for autism.

60 Seconds of Data Now. A Month of Clarity Later.

After Each Session

3 Fields Only

Field 1 — Engagement Rating

Circle one:

😴 Low | 😐 Moderate | 😊 High | 🤩 Very High

Field 2 — Primary Skill Practiced

Check one:

- Counting / Value Recognition

- Saving (adding to jar, progress toward goal)

- Division (Save/Spend/Give allocation)

- Earning (job completed, earnings recorded)

- Trade-off Decision (chose between options within budget)

- Shopping Practice (price comparison, making change)

Field 3 — One Observation

"Today [child] did / said / showed ___________"

Example: "Today Arjun independently put coins in the jar without prompting for the first time."

📋K-913 Progress Tracker — Google Form — Tracks: date, session length, skill level, engagement, parent notes — auto-compiled to shareable report

📊GPT-OS® Integration: Log in GPT-OS® Dashboard → Life Skills → Financial Planning → K-913. Your data feeds your child's AbilityScore® Life Skills Index and informs TherapeuticAI® recommendations.

📊GPT-OS® Integration: Log in GPT-OS® Dashboard → Life Skills → Financial Planning → K-913. Your data feeds your child's AbilityScore® Life Skills Index and informs TherapeuticAI® recommendations.

"60 seconds of data now saves hours of guessing later." — Pinnacle Clinical Principle

Most Sessions Aren't Perfect. That's Not Failure — That's Data.

❓ Child refused to engage at all

What happened: Child is not motivated by current goal item, is in an off state, or money = demand association needs rebuilding.

Next time: Check readiness (Card 14). Update goal picture to something child currently desires intensely. Try invitation approach differently — bring the jar to the child's play space.

❓ Child grabbed all the money and ran

What happened: Impulsive response to visible money — this is the exact behavior we're addressing. It's expected at the beginning.

Next time: Use play money only (no real money) until impulse control around money is established. Teach "money stays in jar" as a separate target first.

❓ Child became upset when they couldn't spend savings immediately

What happened: Delayed gratification is hard. The gap between wanting and having created frustration.

Next time: Reduce goal distance — pick a goal that is only 3–5 days away. Increase visibility of progress (add a progress sticker every deposit).

❓ Child couldn't understand the division concept at all

What happened: Save/Spend/Give requires categorical thinking that may not be ready yet.

Next time: Step back to single-jar saving for one concrete goal only. Add division system only when single-jar saving is mastered.

❓ Child spent all the money before the session started

What happened: Money arrived in hands before structure was established.

Next time: The moment money enters the home, immediately do the division ritual — BEFORE the child takes the money to their room. The structure must happen at point of receipt.

❓ Child has no interest in any goal item to save for

What happened: Abstract saving (for no specific goal) is even harder. The goal picture is motivational infrastructure.

Next time: Spend time identifying what the child currently wants most. Present options: "Would you save for [X] or [Y]?" Physical picture of the item is essential.

"Session abandonment is not failure. It is data telling you what to adjust." — Pinnacle ABA Principle

No Two Children Learn Money the Same Way. Here's How to Adjust.

🔵 For Children with Autism (Concrete Thinkers)

- Use actual physical money, not tokens or points

- Make every abstract concept visible (jars, charts, pictures)

- Maintain exact same routine/ritual every session — predictability is motivating

- Tie savings goal to a special interest item — motivation skyrockets

- Longer timelines are fine — a 3-month saving goal is appropriate if the goal is compelling

🟡 For Children with ADHD (Impulse-First Learners)

- Very short goals first (3–5 days maximum initially)

- Physical money in hands LAST (build structure before access)

- Use movement — counting coins while bouncing on therapy ball, standing at chart

- Gamify: "Can you beat your record? Last time you waited 3 days..."

- Use countdown timer → impulse bridges the gap when time is visible

🟢 For Children with Intellectual Disability

- Focus on functional skills only: recognizing amounts, making simple purchases

- Use picture-based price cards (pictures of items, not abstract prices)

- Simplify to two categories only (Save / Spend) before introducing Give

- Use real coins for tactile recognition — practice sorting by size/color before value

- Celebrate every single small step (5-second coin recognition = a win)

🔴 For Sensory-Sensitive Children

- Let child handle all materials before any financial activity begins

- Some children dislike paper note texture — use coins only, or laminated play money

- Avoid shiny metallic finishes if child has visual sensory sensitivity

- Let child position themselves (standing, sitting on floor) as preferred

Age Range | Focus | Materials | |

5–7 years | Accumulation + counting only | Clear jar + play coins | |

8–10 years | Division + goal-setting | Save/Spend/Give + earning chart | |

11–12 years | Trade-offs + comparison | Budget chart + price cards + shopping games | |

13–14 years | Independence + real decisions | Full system + bank account introduction |

In Weeks 1–2, You Are Building the Foundation. Progress Is Invisible — But Real.

Week 1–2

Foundation Phase · ~15% Progress

What You WILL Likely See (Realistic)

- Child tolerates the money activity without resistance (even if passive)

- Child is willing to come to the table when invited

- Child can identify savings jar as "mine" with some ownership

- Child can count some coins with support

- Child looks at goal picture with some interest

What You Will NOT See Yet (Normal)

- Spontaneous saving behavior (child hasn't initiated yet — expected)

- Understanding of trade-offs (too early)

- Consistent engagement every session (some sessions will be 30 seconds)

- Correct value comparisons without support

Early Progress Signal to Watch For: "If your child says 'my jar' or touches it voluntarily — that's the first neural anchor forming. That is real progress."

The brain needs repeated exposure before understanding emerges. You are laying a neural pathway, not demonstrating a finished skill. A child who tolerates the jar being on the table in Week 1 is at the same developmental position as a child who fills it independently in Week 8. The pathway between these points is your work in Weeks 2–7.

PMC11506176 — Intervention outcomes emerge across 8–12 week timelines; early phase is tolerance and participation.

Something Is Changing. Your Child's Brain Is Consolidating a New Pattern.

Week 3–4

Consolidation Phase · ~40% Progress

Anticipation

Child asks about the savings jar or mentions it unprompted — the system has become meaningful to them.

Ownership Language

"My money" / "My savings" — using possessives about the system. Psychological ownership has formed.

Reduced Resistance

Sessions start without negotiation. The ritual is becoming familiar and safe.

Progress Awareness

Child notices when the jar is fuller / points to goal picture. Visual feedback is registering.

Beginning of Restraint

Pauses before spending impulsively (even if they still spend). The pause is the skill emerging.

When to Increase Frequency or Intensity: If child is showing 3+ consolidation indicators → introduce the next element. Was doing single jar? Add Save/Spend/Give. Was doing division? Add price comparison cards. Was doing price cards? Try a structured shopping game.

Parent Milestone: You may notice you are also more confident. The ritual is becoming automatic for you too. This is the caregiver competence effect — and it matters enormously for your child's outcomes.

The Skill Is Becoming Their Own. Watch for These Mastery Markers.

Week 5–8

Mastery Approaching · ~75% Progress

Money Finitude

Child says "I don't have enough" independently — without being told. ☐ Achieved

Trade-off Awareness

Child hesitates before spending, considers alternatives. ☐ Achieved

Saving Behavior

Child voluntarily adds to jar without prompting at least once. ☐ Achieved

Division Habit

Child reaches for Save/Spend/Give system when given money. ☐ Achieved

Earning Initiation

Child asks "what jobs can I do?" when they want something. ☐ Achieved

🏆 Mastery Unlocked — When 4+ criteria are consistently present over 2 weeks:

→ Consider introducing real bank account (with joint access) for advancing learners

→ Explore K-914: Planning for Future | J-855: Planning & Organization | K-920: Decision Making Skills

→ Consider introducing real bank account (with joint access) for advancing learners

→ Explore K-914: Planning for Future | J-855: Planning & Organization | K-920: Decision Making Skills

PMC10955541 | Meta-analysis mastery criteria + BACB mastery standards

You Did This. Your Child Can Manage Money Because You Showed Up.

You spent weeks building a system that makes money visible for your child. You created jars and charts and earning boards. You sat beside them while they counted the same coins for the fifteenth time. You didn't rush. You didn't give up when sessions were 30 seconds. You adapted and returned. And now your child says "I'm saving for [item]" — and means it. That sentence is the result of your work.

Photo Documentation

Child holding saved-up money in front of goal item. A moment worth preserving forever.

Journal Entry

"Today [child] saved ₹___ for ___. It took ___ weeks. They did it." Write it down. This is evidence of growth.

Make the Purchase a Ceremony

When the first savings goal is reached — child pays themselves. Mark the moment intentionally.

Tell Someone

Share with a grandparent, therapist, or the Pinnacle community. Your breakthrough becomes another parent's hope.

Journal Prompt: "What did I notice change in my child over these weeks? What did I notice change in myself?"

🚨 Know the Signs That Mean "Pause and Ask a Professional"

Red Flags: When to Pause and Consult

🚩 Financial Anxiety Developing

Child shows visible distress, fear, or obsessive worry about family finances — asking repeatedly if "we have enough money," appearing anxious at any money discussion. → Separate child's financial learning completely from family financial discussions.

🚩 Hoarding Behavior Escalating

Child is hiding money, refusing to let any money out of their sight, or showing severe distress when money leaves their possession. → This goes beyond saving into anxiety territory. Consult your behavioral therapist.

🚩 Perseveration on Money

Child cannot stop thinking/talking about money in ways that are distressing or disruptive to daily function. → Needs behavioral assessment.

🚩 Meltdowns Triggered by Any Financial Activity

Sessions consistently end in severe emotional dysregulation. → Current approach/pace is not matched to child's readiness. Consult OT or ABA before continuing.

🚩 No Progress After 12 Weeks of Consistent Practice

No indicators from the progress arc are appearing after 3 months of regular sessions. → Child may need a structured clinical financial skills assessment.

Minor concern | Troubleshoot (Card 22) → Adapt (Card 23) → Retry | |

Persistent concern | Book teleconsult via pinnacleblooms.org/book | |

Significant distress | Clinic visit — Center locator at pinnacleblooms.org/centers | |

Emergency dysregulation | Stop session. Wait. Call 9100 181 181 |

📞FREE: 9100 181 181 — Pinnacle National Autism Helpline | Available 24×7 in 16+ languages | "Trust your instincts. If something feels wrong, pause and ask."

You Are Not Done — You Are at a Junction. Here's Where to Go Next.

→ Path 1: K-914 — Planning for Future

If your child is now managing money at a basic level and you want to extend to broader life planning — career awareness, living arrangements, independence milestones.

→ Path 2: J-855 — Planning & Organization

If your child struggles with the executive function components of financial skills — can't maintain the system, forgets the routine, loses track of progress.

→ Path 3: K-920 — Decision Making Skills

If your child is ready to advance from financial decisions to broader independence decision-making across all life domains.

Long-Term Developmental Goal: Financial independence readiness — measured by GPT-OS® Independence Readiness Index. K-913 is one building block in a multi-year journey toward adult-ready money management. WHO/UNICEF developmental trajectory framework | Domain-specific sequencing literature

Other Life Skills Techniques Your Child May Benefit From

K-912 — Insurance Navigation 🔵 Intro-Level

📦 Documentation Materials — For parents navigating therapy funding and systems. The essential companion to financial planning.

K-914 — Planning for Future 🟡 Core-Level

📦 Planning Tools — Extending financial skills to life planning. The recommended next step after K-913 mastery.

K-911 — School Advocacy 🟢 Core-Level

📦 Communication Boards — Supporting school funding and IEP navigation. Critical for parents navigating educational systems.

K-907 — Tracking Progress 🔵 Intro-Level

📦 Data Tracking Tools — Building systematic progress monitoring. If you have a savings jar, you already have materials for this.

K-906 — Goal Setting 🟡 Core-Level

📦 Visual Goal Systems — Setting meaningful goals your child owns. Same system, extended application beyond money.

K-905 — Data Collection 🟢 Core-Level

📦 Recording Systems — Parent data collection for therapy review. Strengthens the tracking habit you're building in K-913.

Financial Planning Is One Piece of a 12-Domain Developmental Journey

K-Domain Status: Life Skills & Independence

- K-913: Financial Planning — ✅ Active

- K-912: Insurance Navigation — Available

- K-914: Planning for Future — Next Recommended

- K-920: Decision Making — Upcoming

How This Connects to the Bigger Picture

Financial planning feeds directly into C-Domain (managing frustration of wanting vs. having), D-Domain (impulse control around spending), J-Domain (mathematical reasoning applied to life), and G-Domain (independent daily life management). No domain is an island.

WHO NCF Five Components of Nurturing Care | UNICEF 2025 Country Profiles

They Started Where You Are. Here's Where They Got To.

💬 "The jar made saving real. He could see it. He could touch it. He could count it. Abstract became concrete." — Rohan's mother, Pinnacle Network

Rohan, 11 years · Autism + ADHD · Hyderabad

Before: Rohan received his allowance every Sunday. By Sunday evening, it was gone — spent on the first thing he saw, often something he didn't even want an hour later. "We can't afford that" was meaningless to him. He thought the ATM just gave money whenever you needed it.

What they did: Started with a single clear jar with a picture of a Lego set he wanted. Each Sunday, his mother helped him count his money, put it in the jar, and count how many more weeks.

After (10 weeks): Rohan is currently saving for a bicycle — 6 weeks in. Last week, a relative offered him ₹200. Without prompting, he said: "Can I put it in my bicycle jar?" His mother said she cried.

From the Therapist's Notes: This is the visual feedback loop at work — accumulation visible + goal anchored = delayed gratification becomes manageable.

Priya, 9 years · Intellectual Disability · Chennai

Before: Priya had no concept of money value. She would offer ₹2 to pay for a ₹200 item and be confused when the shopkeeper didn't accept it.

What they did: Started with coin sorting only — not buying, not saving. Just identifying ₹1, ₹2, ₹5, ₹10 by size and color. Then play store with price tags of ₹1, ₹2, ₹5 only.

After (12 weeks): Priya can independently make purchases up to ₹50 at the neighborhood store. She picks items, checks the price, counts her coins, and receives change. The shopkeeper knows her.

💬 "She walked in, picked her biscuits, counted her coins, and handed them over. I stood outside. That was the first time in her life she did something completely independently in the world." — Priya's father

Illustrative case. Outcomes vary by developmental profile, consistency, and intervention approach.

"Financial skills feel impossibly far away when a child can't understand why the jar needs to stay closed until the goal is reached. But the concrete-to-abstract progression is real and predictable. A clear jar is not just a jar — it's the child's first experience of delayed gratification made visible." — Pinnacle Occupational Therapist, Life Skills Specialist

50,000+ Families Are Working on This Same Goal. You Don't Have to Figure It Out Alone.

💬 WhatsApp Community — Life Skills & Independence

4,200+ parents sharing earning chart templates, savings jar photos, breakthrough moments, and advice on financial skill milestones.

unknown link

💻 Online Forum — Pinnacle Parent Network

Searchable threads: "My child finally saved enough for the first time" | "Which earning chart works for ADHD?" | "Save-Spend-Give — how to start"

📍 Local Pinnacle Parent Meetups

Monthly meetings at 70+ centers across India — facilitated by Pinnacle therapists, parent-led. Find your nearest center meetup on the center locator.

🤝 Peer Mentoring — Ask an Experienced Parent

Connect with a parent who is 12–18 months ahead on the financial skills journey. Share what worked. Shortcut the learning curve.

→ Request Peer Mentor via 9100 181 181

"Over 1000 individuals from 111 countries contributed to the WHO Nurturing Care Framework. Community engagement is a core principle of effective child development support." — WHO NCF Community Principle

Home + Clinic = Maximum Impact. Here's How to Connect.

Therapist Matching for K-913

Financial planning life skills are led by a coordinated team:

🦾 Occupational Therapist — Life Skills Specialist

Primary lead. Adaptive behavior and executive function components of money handling.

📚 Special Educator — Financial Math & Functional Skills

Mathematical reasoning integrated into real-world functional practice.

🧠 ABA/BCBA — Earning Systems & Impulse Control

Delayed gratification training and behavior-to-reward chains.

👨⚕️ NeuroDev Pediatrician — Developmental Readiness

Baseline assessment, executive function profiling, and milestone monitoring.

Book Your Support

Available in 16+ languages. Same-day slots available.

📍 70+ centers across India

Andhra Pradesh · Telangana · Tamil Nadu · Karnataka · Maharashtra · Delhi · and 20+ more states

Andhra Pradesh · Telangana · Tamil Nadu · Karnataka · Maharashtra · Delhi · and 20+ more states

📞FREE National Autism Helpline: 9100 181 181

No appointment needed. Available 24×7.

"Start here if you're unsure where to begin."

No appointment needed. Available 24×7.

"Start here if you're unsure where to begin."

WHO Progress Report (2023): 48% increase in countries adopting ECD policies. Primary health care identified as key platform for reaching all families.

The Evidence Base Behind K-913 — For the Curious and the Skeptical

📚 WHO Care for Child Development (CCD) Package

Home-based caregiver-delivered interventions using concrete materials across 54 low/middle-income countries showed equivalent outcomes to clinic-based approaches for life skills acquisition.

Ref: PMC9978394 | WHO/UNICEF CCD Package (2023) — → Read on PubMed

📚 PRISMA Systematic Review — Sensory & Behavioral Interventions

16 articles (2013–2023) confirm structured intervention meets evidence-based practice criteria for autism. Visual, concrete, hands-on approaches show effectiveness across adaptive behavior domains.

Ref: PMC11506176 — → Read on PubMed

📚 Meta-Analysis — Adaptive Behavior Interventions (2024)

24 studies confirm effectiveness of structured life skills interventions for promoting adaptive behavior, functional independence, and social skills.

Ref: PMC10955541 | World J Clin Cases 2024 — → Read on PubMed

📚 Indian RCT — Home-Based Structured Interventions (Padmanabha et al., 2019)

Indian families administering structured home-based interventions showed significant developmental outcomes across adaptive behavior domains including life skills.

Ref: DOI:10.1007/s12098-018-2747-4 | Indian J Pediatr 2019 — → Read full study

📚 NCAEP Evidence-Based Practices Report (2020)

Visual supports, video modeling, and token economy systems are classified as evidence-based practices for autism — all three are core components of the K-913 financial skills protocol.

Ref: National Clearinghouse on Autism Evidence and Practice (2020) — → NCAEP Report

Your Data Makes Your Child's Plan Smarter. Here's How.

What GPT-OS® Learns from K-913 Data

- Which stage of financial understanding your child is at (foundational/emerging/developing/advancing)

- Whether delayed gratification tolerance is improving (milestone detection)

- Optimal session frequency for your child's engagement profile

- Whether to accelerate to K-914 or strengthen K-913 further

- Cross-domain connections (K-913 progress feeding D-domain impulse control profile)

Population-Level Impact

Every family contributing K-913 data improves the algorithm for every similar child. When 10,000 families track financial skills progress through GPT-OS®, the recommendations for the 10,001st family become dramatically more accurate.

Privacy Assurance

🔒 All data encrypted and anonymized for population analysis

🔒 Individual data visible only to you and your designated therapist

🔒 Compliant with Indian PDPB framework and international standards

🔒 Individual data visible only to you and your designated therapist

🔒 Compliant with Indian PDPB framework and international standards

GSTIN Registered: 36AAGCB9722P1Z2 | CIN: U74999TG2016PTC113063

The Original Reel That Surfaces This Challenge

🎬 Reel ID: K-913

Life Skills & Independence · Episode 913

⏱️ 75–85 seconds

Reel Learning Objectives

After watching this 75-second reel:

- ✅ Parent can name all 9 materials

- ✅ Parent understands why each makes money concrete

- ✅ Parent has a starter purchase plan (₹0–₹800)

- ✅ Parent knows the developmental sequence for introducing materials

Video shows: Clear savings jar accumulation · Play money counting · Budget chart allocation · Earning chart system · Price comparison cards · Shopping practice game · Countdown calendar · Financial storybook · Save-Spend-Give dividers

Adjacent Reels

Video Modeling Evidence: NCAEP (2020) — Video modeling is evidence-based practice for autism. Multi-modal learning (visual + text + demonstration) improves parent skill acquisition.

One Parent Doing This Creates Some Impact. The Whole Family Doing It Creates Transformation.

"Consistency across caregivers multiplies impact. One caregiver doing this at 70% consistency has less effect than three caregivers doing it at 50% consistency each. Shared knowledge is therapeutic infrastructure."

For Your Spouse / Partner

💬 "I've been learning a structured approach to teaching [child's name] about money. It uses visual jars and charts instead of explanations. Takes 15 minutes a day. The consistency between both of us matters enormously. Here's the page — can you read Cards 14–20 today?"

For Grandparents (Simplified)

"[Child's name] is learning about money using a system of jars and charts. When [he/she] gets money, it goes into the jar FIRST before anything can be spent. Please don't give [child's name] money to spend directly — help [him/her] put it in the jar instead. This is part of [his/her] therapy program."

For Teachers / School

Subject: Financial Life Skills Program — Please Support at School. "[Child's name] is working on a structured financial literacy program as part of [his/her] OT/life skills plan. At home we use a visual saving system and an earning chart. If there are any school shop or money-handling opportunities, please use the attached approach guide."

PMC9978394 — Multi-caregiver training as critical for intervention generalization and maintenance.

Your Questions, Answered by the Pinnacle Consortium

❓ At what age should I start financial skills teaching?

Start as early as age 3–4 with simple coin identification and "money goes in the bank" concepts. The materials on this page are calibrated for ages 5–14. The foundational stage (3–5) is appropriate even before formal therapy targets are set. Earlier is better — but it's never too late.

❓ My child has autism and doesn't understand numbers at all. Is this page relevant?

Absolutely. The number-matching stage (recognizing ₹1 vs ₹5 by size/color, not value) is the appropriate starting point. The progression from sorting by appearance to understanding value to making purchases is well-documented and achievable. Start at the beginning.

❓ Should I give an allowance? How much?

Regular, consistent allowance is the most effective teaching tool because it provides predictable practice. Amount: enough to require choices (can't buy everything). Typical range: ₹10–50/week for ages 5–8; ₹50–200/week for ages 9–14. Consult your OT for child-specific guidance.

❓ My child spends any money they see immediately. Won't giving them money just make this worse?

This is the insight behind the system: the division ritual must happen at the point of receipt. Money never reaches the child's pocket directly — it goes to the jar/division system first. Impulsive spending is a symptom; the ritual-based system is the treatment. Work through the 6-step protocol consistently. Impulse behavior will decrease over weeks.

❓ How do I handle gift money from relatives?

Use the Grandparent Guide (Card 38). Brief relatives: "All of [child's name]'s money goes into the savings system. Please give it to us/to the jar directly." If money is given directly, do the division ritual immediately together before any spending happens.

❓ How long until I see real progress?

Realistic timeline for foundational understanding (money is finite, saving is possible): 6–10 weeks of consistent practice. Behavioral independence (saving without prompting, basic budgeting): 3–6 months. Full age-appropriate financial competency: 12–24 months. Progress is real from Day 1 — the tolerance to engage is the first step.

❓ I've tried this before and it didn't work. Why should I try again?

If previous attempts didn't work, something in the approach didn't match your child's readiness level, motivation, or environmental setup. This is data. The troubleshooting and adapt-and-personalize cards address the most common mismatch patterns. Consider a single OT consultation before restarting — 30 minutes of professional insight can save months of misdirected effort. (📞 9100 181 181)

Preview of 9 materials that help with financial planning Therapy Material

Below is a visual preview of 9 materials that help with financial planning therapy material. The pages shown help educators, therapists, and caregivers understand the structure and content of the resource before use. Materials should be used under appropriate professional guidance.

Link copied!

One Clear Jar. One Goal Picture. That's All You Need to Start Today.

The entire financial skills journey begins with a child watching coins accumulate toward something they want. Start there. Today.

🦾 Occupational Therapy

Life Skills Specialist — Primary Lead

🧠 ABA / BCBA

Earning Systems & Delayed Gratification

📚 Special Education

Financial Math & Functional Skills

👨⚕️ NeuroDev Pediatrics

Developmental Readiness & Trajectory

🏛️ Pinnacle Blooms Network® — The Pinnacle Promise

Built by Mothers. Engineered as a System. From fear to mastery. One technique at a time.

OT • SLP • ABA/BCBA • SpEd • NeuroDev • CRO • WHO/UNICEF-Aligned • DPIIT Recognized

20M+ sessions | 97%+ measured improvement | 70+ centers | GPT-OS® governed

Built by Mothers. Engineered as a System. From fear to mastery. One technique at a time.

OT • SLP • ABA/BCBA • SpEd • NeuroDev • CRO • WHO/UNICEF-Aligned • DPIIT Recognized

20M+ sessions | 97%+ measured improvement | 70+ centers | GPT-OS® governed

🔄Loop continues → K-914: 9 Materials That Help Planning for Future

Medical Disclaimer: This content is educational and informational. It does not constitute medical advice and does not replace individualized assessment and intervention from qualified developmental therapists, occupational therapists, life skills specialists, or medical professionals. Children with developmental differences may require adapted approaches and extended timelines. Individual outcomes vary based on child profile, developmental stage, and intervention consistency. Consult your child's professional therapy team for personalized programming.

📞9100 181 181 (FREE, 24×7, 16+ languages) | 🌐pinnacleblooms.org | care@pinnacleblooms.org | 📍 70+ centers across India

CIN: U74999TG2016PTC113063 | DPIIT: DIPP8651 | MSME: TS20F0009606 | GSTIN: 36AAGCB9722P1Z2

© 2025–2026 Pinnacle Blooms Network®, a unit of Bharath Healthcare Laboratories Pvt. Ltd. | Technique K-913 | GPT-OS® Content Intelligence System

CIN: U74999TG2016PTC113063 | DPIIT: DIPP8651 | MSME: TS20F0009606 | GSTIN: 36AAGCB9722P1Z2

© 2025–2026 Pinnacle Blooms Network®, a unit of Bharath Healthcare Laboratories Pvt. Ltd. | Technique K-913 | GPT-OS® Content Intelligence System